For many students, getting accepted to college feels like crossing the finish line. In reality, it’s the beginning of one of the biggest financial decisions they will ever make.

The cost of higher education continues to rise, and students today are faced with a complicated mix of tuition bills, financial aid packages, scholarships, grants, work opportunities, and student loans. While college can be a worthwhile investment, the way students choose to pay for it can have long-term consequences that extend far beyond graduation.

The good news? Students don’t have to choose between attending college and being financially responsible. With the right planning and knowledge, they can minimize debt, maximize available resources, and make informed decisions that support their future financial well-being.

Start with the True Cost of College

One of the most common mistakes students make is focusing only on tuition when comparing colleges. The actual cost of attendance includes much more:

- Tuition and fees

- Housing and meal plans

- Textbooks and supplies

- Transportation

- Technology and equipment

- Personal expenses

Before committing to a school, students should calculate the total annual cost and compare it with the financial aid offered. A college that appears more expensive at first glance may actually be more affordable after scholarships and grants are applied.

Students should also think beyond the first year. Financial aid packages can change, and some scholarships may only be available for a limited period. Understanding the four-year cost of a degree can help prevent financial surprises later.

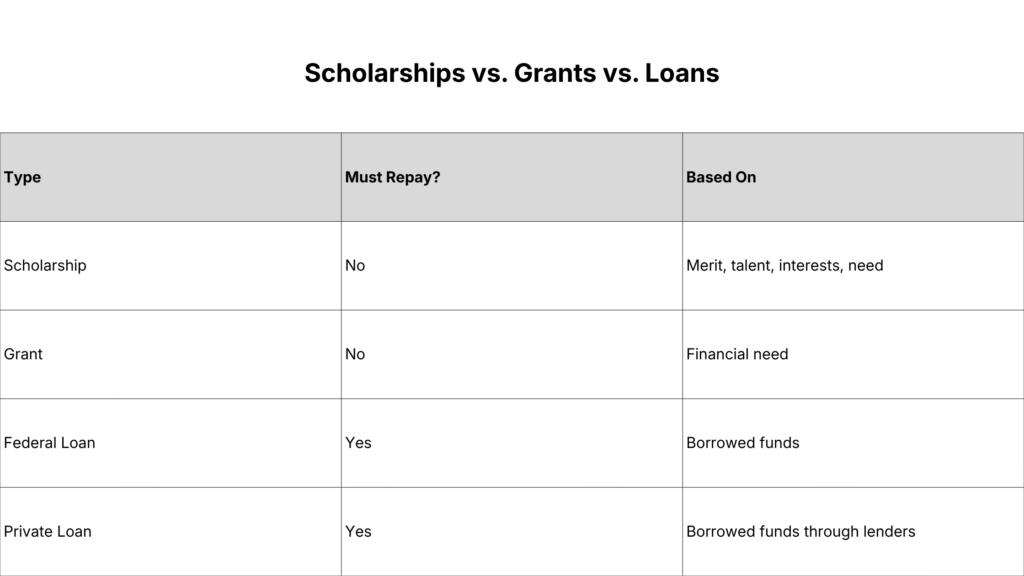

Prioritize Free Money First

When paying for college, the smartest money is money that doesn’t need to be repaid. Students should always maximize sources of free financial aid before considering loans. These include:

Grants: Grants are typically awarded based on financial need and do not need to be repaid. Completing the FAFSA (Free Application for Federal Student Aid) is often the first step in determining eligibility for federal, state, and institutional grants. Many students mistakenly assume they won’t qualify for aid and skip the FAFSA altogether. In reality, millions of dollars in aid go unclaimed every year because students don’t apply.

Scholarships: Scholarships are another powerful way to reduce college costs. Unlike loans, scholarship funds are essentially investments in a student’s future that never need to be repaid. Scholarships are available for:

- Academic achievement

- Community service

- Leadership

- Athletics

- Artistic talents

- Career interests

- Cultural backgrounds

- Financial need

- Specific majors or industries

The key is applying consistently and broadly.

Where Students Can Search for Scholarships

Finding scholarships requires effort, but the potential payoff is enormous. Students should start searching as early as possible and continue throughout college.

Fastweb

One of the largest scholarship databases available, Fastweb matches students with scholarships based on their background, interests, and academic profile.

Scholarships.com

This platform allows students to create profiles and receive customized scholarship recommendations.

College Board Scholarship Search

The organization behind the SAT also maintains a comprehensive scholarship database with thousands of opportunities.

CareerOneStop Scholarship Finder

Sponsored by the U.S. Department of Labor, this resource offers a searchable database of scholarships, grants, and financial aid opportunities.

Local Opportunities

Many students focus exclusively on national scholarships and overlook local awards, which often have fewer applicants. Students should check with:

- High school counseling offices

- Community foundations

- Local businesses

- Credit unions and banks

- Civic organizations

- Religious organizations

- Employers

- Professional associations

A $500 or $1,000 local scholarship may seem small compared to a full-tuition award, but multiple smaller scholarships can add up quickly and significantly reduce borrowing needs.

Be Strategic About Student Loans

Student loans can make college possible for many students, but they should be approached carefully.

Borrowing isn’t inherently bad. In fact, responsible borrowing can help students invest in education while building a foundation for future earning potential. Problems arise when students borrow more than they can realistically afford to repay. Before accepting any loan, students should ask themselves:

- How much am I borrowing in total?

- What will my monthly payment be after graduation?

- What is the interest rate?

- How long will repayment take?

- What salary can I reasonably expect in my chosen field?

These questions help students understand the true cost of borrowing before signing loan agreements.

Understand the Difference Between Federal and Private Loans

Not all student loans are created equal.

Federal Student Loans

Federal student loans generally offer more borrower protections and flexible repayment options than private loans. Benefits may include:

- Fixed interest rates

- Income-driven repayment plans

- Deferment and forbearance options

- Potential forgiveness programs

- Consumer protections

Because of these advantages, financial aid experts generally recommend exhausting federal loan options before considering private loans.

Private Student Loans

Private loans are offered by banks, credit unions, and other lenders. While they can help fill funding gaps, private loans often have:

- Higher interest rates

- Fewer repayment protections

- Credit requirements

- Co-signer requirements

Students should carefully compare terms and only borrow what is absolutely necessary.

Follow the “Borrow Less Than Your First-Year Salary” Rule

A common guideline for responsible borrowing is to avoid taking on more student debt than the expected first-year salary in your chosen career.

For example:

- A student expecting to earn $50,000 after graduation should aim to keep total student loan debt below $50,000.

- A student entering a field with a $40,000 starting salary should ideally borrow less than $40,000.

While this isn’t a perfect formula, it provides a useful benchmark for maintaining manageable repayment obligations.

Consider Work Opportunities During College

Working while attending school can help students reduce borrowing and gain valuable experience. Options include Federal Work-Study programs, campus jobs, internships, part-time employment, or even something like tutoring.

Earning just a few thousand dollars annually can help cover textbooks, transportation, or personal expenses that might otherwise end up on a student loan balance.

In addition to financial benefits, work experience can strengthen a student’s resume and improve employment prospects after graduation.

Be Careful About Lifestyle Inflation

College spending isn’t limited to tuition bills. Many students unintentionally increase their financial burden through discretionary spending on:

- Dining out

- Entertainment

- Travel

- Subscription services

- New technology

- Credit card debt

Learning to budget during college can make a meaningful difference. Students don’t need to eliminate all fun or social activities, but understanding the difference between wants and needs can help prevent unnecessary borrowing. Every dollar not spent today is one less dollar that may need to be financed through loans tomorrow.

Reevaluate Every Year

Paying for college should not be a one-time decision. Students should review their financial situation annually and ask things like are there new scholarships available? can I reduce expenses? and have my career goals changed?

Many scholarships are available specifically for current college students, yet they often receive fewer applications than scholarships aimed at high school seniors. Continuing the scholarship search throughout college can significantly reduce total borrowing.

Building Financial Responsibility Starts Now

The decisions students make about paying for college can influence their financial lives for years after graduation.

Being financially responsible doesn’t necessarily mean avoiding student loans altogether. It means understanding the options, maximizing free financial aid, borrowing strategically, and maintaining a long-term perspective.

Students who prioritize scholarships, take advantage of grants, work when possible, and borrow thoughtfully are often better positioned to achieve financial stability after graduation. College is an investment in the future. The goal isn’t simply to earn a degree, it’s to earn that degree in a way that supports future financial success rather than creating unnecessary financial obstacles.

By approaching college funding with knowledge, planning, and discipline, students can graduate with both an education and a strong financial foundation for the next chapter of their lives.